We are a leading, management-owned research boutique with a focus on companies from Europe. Our role is that of an intermediary between companies on the one hand and investors on the other.

Our research products are directly distributed to more than 200 mutual and pension funds, family offices and independent asset managers from Central and Eastern Europe, the German-speaking region, Scandinavia, France and UK. In addition, we publish our reports on platforms such as Thomson Reuters, Capital IQ, Factset, Researchpool.com, rsrchxchange.com, ERI-C.com, Visiblealpha.com, ISBNews and PAP, thus ensuring that they are available to institutions from around the world. By organising roadshows and conferences, we provide investors with direct access to corporate decision makers.

Our team consists of professionals with long capital market experience in both Western Europe and the CEE region.

Team

Adrian Kowollik

Adrian Kowollik is Managing Partner at East Value Research and the analyst covering the sectors Technology/Media/Telecom, IT, E-Commerce and Health Care. He graduated in Business Administration from Humboldt University in Berlin and has more than 8 years of experience in equity research and corporate finance. Adrian, who grew up in both Poland and Germany, is a strong believer in the concept of broker-independent equity research and the advantages, which it provides to both companies and investors. Linkedin profile

Mateusz Pudlo (Analyst)

Mateusz Pudlo is Analyst. He has a Bachelors‘s degree in Accounting and Finance from the Wroclaw Business School and a Master’s degree in Economics and Business from Erasmus School of Economics in Rotterdam. His tasks include the preparation of sector reports, company analyses and valuations. Previously, he worked as Assistant in Accounting at EY (Polish branch).

Yusuf Bilgic (Advisor)

Yusuf Bilgic is Advisor to East Value Research. During his impressive career, he was among others Managing Director, Head of Equity Sales & Equity Sales Trading at Lampe Capital in London (previously, part of the German Oetker Group); Director Equity Sales at the oldest German private bank Bankhaus Metzler in Frankfurt; and Vice President Cash Equity Sales Trading at Banco Santander in Frankfurt. Among his clients were institutional investors incl. long/short hedge funds from continental Europe, UK and the United Arab Emirates. Yusuf is based in London.

Michael Lexa (Advisor)

Michael Lexa is Advisor to East Value Research. He looks back at a successful career as Equity Sales among others at Centrobanca, Julius Baer and Dresdner Bank. Over the last 30 years, Michael, who is based in Milan, has been introducing Italian listed companies to DACH-based institutional investors.

Services

Research

We provide broker-independent research on companies that are headquartered in Europe. Our main focus is on small-, micro- and nanocaps, an area, which is usually below the radar of typical brokerage houses. Scientific studies have shown that broker-independent research can be very helpful for companies when it comes to increasing their market visibility and liquidity.

In addition to analysis of single companies, which can be either sponsored or fully independent, we also offer sector reports, whereby we leverage our sector expertise and knowledge of markets in Western and Eastern Europe. Investors can gain access to all our past and future research reports through 1. the relevant research platforms and 2. by purchasing a yearly subscription on our website.

Roadshows

For the companies, which we cover, we organise international roadshows. Thus, we provide them with access to new investor groups and help to diversify the shareholder structure. Through our broker partners, we can also act as an intermediary in capital market transactions.

Consulting for Start-ups

In addition to services for listed companies, we also offer advisory for European start-ups, especially when it comes to raising capital in CEE and Western markets.

Valuation Services & Corporate Finance

Our offering is complemented by valuation services as well as corporate finance advisory, which we are able to offer our clients through our partnership with the Berlin-based firm InveSP Capital Partners. InveSP Capital Partners provides M&A, restructuring and financing advisory services for smaller companies from Western and Eastern Europe. In the last years, it has completed transactions worth EUR >1bn, many of which were crossborder deals.

Imprint

East Value Research GmbH Gontardstr. 11 10178 Berlin Germany Tel.: +49 30 20609082

E-Mail: kontakt@eastvalueresearch.com Represented by: Adrian Kowollik Commercial Register: Registration at Amtsgericht (District Court) Berlin-Charlottenburg under the registration number HRB 164473 B. VAT-Id: DE298268078

Copyrights All rights reserved. Reproduction, commercial redistribution and entry into commercial databases are only allowed with the written consent of East Value Research GmbH.

Liability This website www.eastvalueresearch.com has been prepared with the greatest possible care. However, East Value Research GmbH cannot guarantee that the information contained herein is correct or precise. Any liability for damages, which result directly or indirectly from the use of this website, will not be assumed if it is not intentional or reckless. If there are links to external websites, East Value Research GmbH will not take the responsibility for their content.

Conflicts of interest East Value Research GmbH has taken several measures to prevent conflicts of interest. One of these is that its employees are prohibited to trade in stocks from its coverage that is being sponsored e.g. by issuers. In addition, its employees are not permitted to accept gifts or any other beneficial contributions from individuals, who have an interest in the content of our research publications.

This blog post is the latest chapter in our ongoing series analyzing Polish companies alongside their listed German counterparts. Today, we take a closer look at two leading e-commerce players specializing in the distribution of bicycles and related accessories.

History & current business

Dadelo was established in 2016 and became part of the Oponeo.pl S.A. Group in 2017, before being spun off and listed on the Warsaw Stock Exchange in 2020. The company remains closely linked to its parent, sharing key management — including Oponeo co-founder Ryszard Zawieruszy?ski — and is headquartered in Bydgoszcz, Poland. Since its public debut, Dadelo has grown to become one of the leading online retailers in the Polish bicycle market. With 17,500 m² of warehouse space, the company offers 85,000 selected products across 520 brands and employs over 200 people. Dadelo conducts its e-commerce operations through its own website, CentrumRowerowe.pl, and maintains four physical stores in major Polish cities. Currently, the company operates exclusively within its domestic market.

Dadelo’s growth strategy includes opening new physical stores in all Polish cities with populations over 200,000, aiming to create a nationwide network where the distance between any two stores does not exceed 200 km. According to the CEO, this expansion is expected to be completed within three years. While brick-and-mortar stores currently account for only a small share of total revenue — and at lower margins — they are the main sales channel for bicycles, which now represent nearly 50% of total revenue. For many customers, purchasing a bicycle is a significant investment, and the ability to see and test-ride the product in person remains a key factor in the buying decision.

Bike24 was founded in 2002 in Dresden, Germany, by Andrés Martin-Birner, Falk Herrmann, and Lars Witt. The company has grown into one of continental Europe’s leading e-commerce platforms for bicycles, with a strong presence in the DACH region (Germany, Austria, Switzerland). After a period under private equity ownership, Bike24 went public via an IPO on the Frankfurt Stock Exchange in 2021. In contrast to Dadelo’s focused domestic approach, Bike24 has pursued broad international expansion and now serves customers in over 70 countries through its main platform and 10 localized websites in key markets such as Spain, France, and Italy. The company employs over 500 people.

To support its extensive operations, Bike24 operates a primary logistics centre near Dresden and a second logistics hub in Barcelona, Spain (10,000 m²), aimed at improving service in Southern European markets. Its product offering includes over 70,000 carefully selected items from more than 800 brands.

The strategy of the German counterpart focuses on expanding into continental European markets through organic growth, although management does not rule out opportunistic acquisitions. This approach emphasizes localization by providing websites in national languages, integrating local and customary payment systems, and offering region-specific customer service.

In contrast to Dadelo, Bike24 operates without a physical retail network—aside from a single store in Dresden and a service point in Berlin — and is fully focused on e-commerce. Bike24 formally entered into direct competition with Dadelo’s online business in 2025 when it launched its Polish website. However, the platform currently accepts only euro payments and does not support BLIK, Poland’s most popular online payment method — factors that may discourage local consumers and limit market adoption.

Historical & current financials

Dadelo has demonstrated an impressive growth trajectory, increasing its revenues from PLN 64.5m in 2020 to PLN 280.5m in 2024, representing a CAGR of 44.4%. This growth has been driven by strong sales of both traditional and electric bikes, with the company offering popular third-party brands alongside its own in-house brands (Oxfeld and Unity), through both online and offline channels.

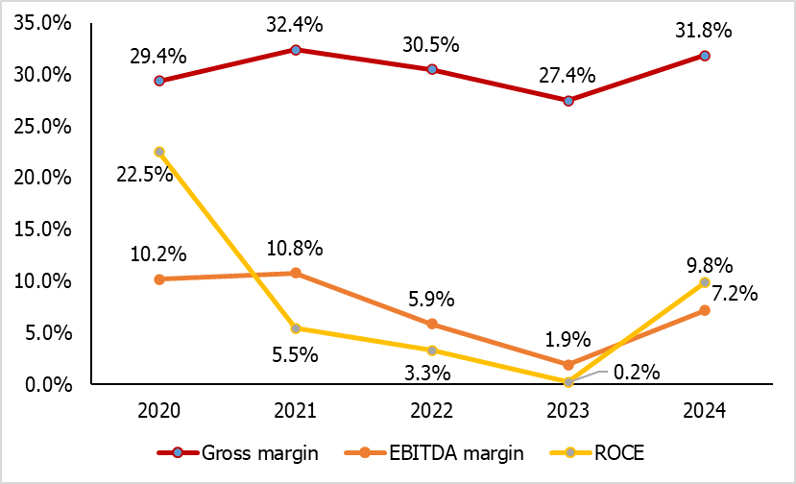

The share of bicycle sales has grown significantly — from 23.1% of total revenue in 2020 to 41.3% in 2024. Physical stores now account for 20–25% of total revenues, while e-commerce contributes the remaining 75–80%. Since its public listing, Dadelo’s EBITDA margin has ranged between 1.9% and 10.8%, while Return on Capital Employed (ROCE) has fluctuated between 0.2% and 22.5%. In 2024, the company fulfilled 648,200 orders, resulting in an estimated average order value of PLN 433 (approximately EUR 101.80).

Dadelo S.A.: Gross & EBITDA margins and ROCE in 2020-2024

Source: East Value Research GmbH, Dadelo S.A.

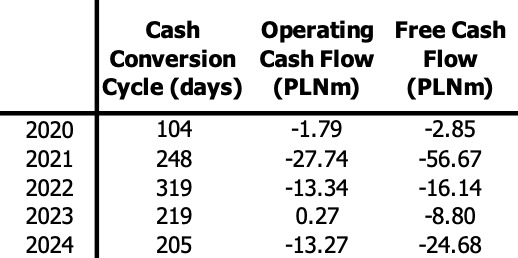

Dadelo S.A.: Cash Conversion Cycle, Operating and Free Cash Flow in 2020-2024

Source: East Value Research GmbH, Dadelo S.A., MarketScreener (for Cash Conversion Cycle)

Over the past three years, Dadelo’s average inventory turnover ratio was 1.38x, compared to 2.49x for Bike24. As a result, Dadelo’s cash conversion cycle is approximately twice as long. While the Polish company’s inventory levels appear reasonable given rising costs and strong growth prospects, maintaining higher inventory levels also increases the risk of obsolescence and potential write-downs—particularly if the market experiences a downturn.

In contrast, its German counterpart maintained relatively lower inventory levels, reducing them by EUR 10.3m in 2024, which contributed to a positive operating cash flow of EUR 7.4m. Despite reporting net income of PLN 11.5m in 2024, Dadelo posted negative operating cash flow of PLN -13.27m, primarily due to a PLN 70m increase in inventories.

As for financial projections, Dadelo’s CEO recently stated in an interview that the company expects to exceed PLN 400m in revenue in 2025E and aims to sustain a robust annual growth rate of 30% over the next five years. Dadelo’s strategic goal is to capture 35–40% of the Polish bicycle and accessories market, which is estimated to be worth PLN 4.5–5bn.

Meanwhile, Bike24 — supported by strong H1 2025 sales — is forecasting up to 15.3% y-o-y revenue growth for 2025E.

Current valuation & conclusion

Both stocks have experienced a remarkable run in 2025, with Dadelo up 162.5% YTD and Bike24 up 168.5% YTD. As a result, both companies are currently trading above their 3-year average EV/Sales multiples.

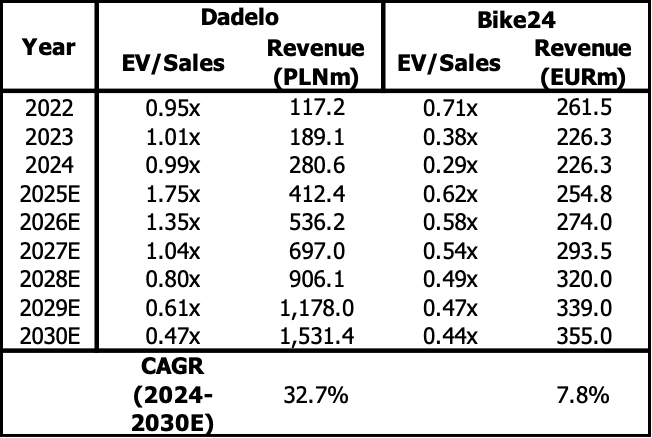

In the table below, we present market estimates of EV/Sales for Bike24, alongside our own calculated EV/Sales for Dadelo. Our calculation is based on the CEO’s projection of 30% annual growth over the next five years, which would result in estimated revenues of PLN 1.5bn by 2030.

Source: East Value Research GmbH (Dadelo 2025E-2030E estimates), CapitalIQ, MarketScreener

While Dadelo’s valuation may appear high compared to its peer Bike24, it is justified by our estimated CAGR of 32.7% for 2024–2030E, versus 7.8% for Bike24. This level of growth, while ambitious, is still below Dadelo’s historical CAGR for 2020–2024. Moreover, we believe the estimates are attainable, given Dadelo’s superior business model and strong management track record.

If Dadelo successfully achieves its domestic targets, the company views expansion into comparable foreign markets—such as the Czech Republic or Hungary—as feasible within a few years. Considering that bike sales are strongly supported by physical retail locations, and with multiple new stores planned over the next three years, along with potential international expansion, we believe the stock could reasonably trade at 2.0x EV/Sales for 2025E. This would imply a share price of over PLN 60.

In the case of Bike24, its lower valuation metrics reflect the company’s underwhelming performance, with revenues showing minimal growth since 2020. Despite a strong share price rally in 2025, the stock continues to trade well below its IPO price from 2021. Additionally, Bike24 still generates a significant portion of its revenue from bike parts, accessories, and clothing—a segment facing intense competition as consumers increasingly turn to lower-cost alternatives, particularly from China.

With both companies reporting strong results for H1 2025, we expect this positive momentum to continue throughout the remainder of the year. However, in the long term, bicycle sales growth rates in both countries are projected to decline. The German market is showing signs of saturation, while in Poland, growth is slowing as pandemic-era demand normalizes.

In an industry where both companies operate, sustaining growth will depend not only on operational excellence and capitalizing on transformative trends — such as the rise of e-bikes — but also on strengthening customer retention in an increasingly competitive market.

Founded in 1998, Grupa Diagnostyka is the leading provider of diagnostic services in Poland, a country that still lags behind the OECD average in terms of health spending per inhabitant and its share in GDP.

Currently, Diagnostyka operates nationwide, with over 1,100 owned and more than 7,000 partner blood collection points, 156 diagnostic laboratories, and 19 diagnostic imaging centers. Each year, the company serves more than 20m customers and conducts over 140m exams. Its service offering includes laboratory exams such as analytical, microbiological (used to detect, identify, and study microorganisms), serological (used to detect and measure the presence of antibodies or antigens in a blood sample), histopathological (analysis of tissue samples), and genetic exams (DNA analysis); diagnostic imaging (ultrasound, computed tomography, magnetic resonance imaging, and remote analysis of diagnostic images for third-party clinics); as well as the collection, analysis, and transport of biological materials for B2B clients, including clinics, doctor’s offices, and research centers, both public and private.

In 2023, the B2C segment contributed approximately 40%, while the B2B segment accounted for around 60% of Diagnostyka’s total revenues, with a retention rate of over 95% in case of institutional clients.

Since 2011, Diagnostyka has grown both organically and through 128 acquisitions, including smaller independent laboratories and diagnostic imaging centers. In the near future, the company plans to focus its investments on further developing its proprietary software, particularly by adding AI functionality. Moreover, as the diagnostic imaging market in Poland remains highly fragmented, with the largest players controlling only around 55% of the market, management plans to focus its M&A activity on this area. The company expects to invest PLN 80m per year in the short term and PLN 70m per year in the medium term.

Financials

According to the company’s IPO prospectus, in 2011-2023 Grupa Diagnostyka has increased its revenues at a CAGR of c. 24% to PLN 1.6bn. In 2023, gross and EBITDA margin equalled 63.9% (2022: 63.8%) and 24% (25.7%) compared to 42.2% and 35.7% respectively at its main Polish peer Voxel, which offers diagnostic imaging services, produces radiopharmaceuticals and distributes software and equipment for radiologistics. Net income declined by 26.3% y-o-y to PLN 123.4m. Operating cash flow amounted to PLN 336m (2022: PLN 283.9m) and the free cash flow to PLN 164.5m (PLN 182.5m).

In 9M/24, Diagnostyka generated revenues of PLN 1.44bn (+22.5% y-o-y), a gross margin of 64.4% (9M/23: 64%), an EBITDA of PLN 378m (+30.3% y-o-y, 26.2% margin) and net income of PLN 169.6m (+80.3%). While the volume of exams increased by 13.3% y-o-y, the average price improved by 8.5%. At the end of September 2024, the company’s net gearing equalled 209.3% and thus was high. However, of the total interest-bearing debt of PLN 869.7m only 14.8% was short-term. Moreover, the net debt-to-EBITDA ratio equalled only 1.8x and in 2021-2023 never surpassed 2x.

IPO & shareholder structure

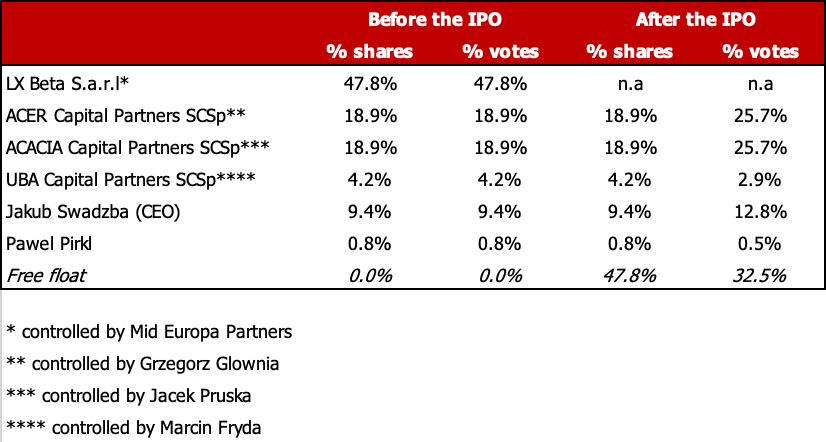

Diagnostyka, which is owned by the CEE-focused private equity fund Mid Europa Partners, announced its IPO on January 13. As part of the transaction, Mid Europa that invested in the company in 2011 is offering 16,147,124 of its shares at the maximum price of PLN 105 per share (IPO value: PLN 1.7bn, implied equity value of 100% of Diagnostyka: PLN 3.5bn). According to Polish media, the order book in the retail tranche was already filled after 1 hour, indicating a strong performance of the stock on the first trading day on February 7th.

Below is an overview over Diagnostyka’s shareholder structure before and after the Initial Public Offering (Source: Diagnostyka’s IPO prospectus). After the IPO, the CEO Jakub Swadzba and other founders will collectively own 47.2% of the company’s shares and 64.1% of its votes.

Summary & conclusion

We believe that Diagnostyka is a company with an excellent track record and growth prospects. According to the OECD, in 2023 Poland only spent USD 2,682.10 per inhabitant on public & private healthcare, which is significantly less than e.g. Germany (USD 5,971.30) or even the Czech Republic (USD 3,227.80). By 2027E, the government plans to increase the share of public health spending in GDP from 6.2% in 2024 to 7% (Source: money.pl). For private health spending, which include e.g. out-of-pocket spending on health, latest forecasts foresee a CAGR 2023-2028E of 10% for the respective value to PLN 54bn (Source: PwC). While in the area of laboratory diagnostics, the market in Poland was valued at EUR 1.6bn in 2023 and its CAGR by 2030E is estimated at 7-9% (Source: Business Insider), the Polish diagnostic imaging market is expected to grow at 7% on average by 2030E from a value of EUR 1.6bn in 2023 (Source: Diagnostyka).

In our view at the max. price of PLN 105 Diagnostyka’s valuation is compelling compared to its main Polish peer Voxel. With 33,756,500 shares outstanding, net debt of PLN 834.3m and trailing EBITDA after 9M/24 of PLN 378m, Diagnostyka would be valued at a trail. EV/EBITDA of 11.6x compared to 12.5x for Voxel, whose current market capitalisation equals PLN 1.5bn.

Based on our analysis, we recommend investors to BUY Diagnostyka S.A.’s shares, which in our opinion represent an attractive long term investment opportunity. We would also like to emphasize that the company’s dividend policy includes a payout ratio of at least 50% of annual net profit going forward.

PKP Cargo is the leading railway cargo company in Poland and the second largest in Europe, serving clients across various sectors including mining, metallurgy, construction, chemicals, food, timber, and automotive. With the largest rolling stock fleet in CEE, including over 1,500 locomotives and more than 52,000 wagons, the company provides stand-alone freight transport in Poland, the Czech Republic, Slovakia, Germany, Austria, the Netherlands, Hungary, Lithuania, and Slovenia. Additionally, PKP Cargo offers forwarding, customs services, transshipment, and delivery to final recipients. The company operates 4 own modernisation facilities and 25 transshipment terminals – 12 of which are intermodal or combine intermodal and conventional functions – with an annual capacity of 1.2m TEU containers. PKP Cargo’s largest shareholder is the Polish state, which holds 33.01% of the shares and effectively controls the company.

Since its IPO on the Warsaw Stock Exchange in 2013, PKP Cargo’s market position — at that time holding a market share of 48.6% in Poland — has significantly weakened to 27.9% after November 2024. In our view, this decline results from both increasing competition, particularly from cargo companies in neighbouring countries, and mismanagement by previous leaders, who were appointed based on political loyalties rather than merit. While Poland’s and the EU’s GDP (in USD) grew at a CAGR of 4.6% and 1.9%, respectively, from 2013 to 2023, PKP Cargo’s revenues increased at an average annual rate of just 1.5% over the same period.

In 2024, PKP Cargo faced a severe liquidity crisis, which forced management to submit an application to the court for the initiation of restructuring proceedings and reduce the Group’s workforce by approximately 18.4% (a total of 3,665 employees). The market consensus is that this was primarily due to a politically motivated decision by former Polish Prime Minister Morawiecki in 2022, combined with excessive and unnecessary expenses (e.g. sponsorships and legal services) incurred by PKP Cargo’s management. In 2022, during the energy crisis, the Polish Prime Minister instructed PKP Cargo to transport coal from abroad to address shortages in Poland. To free up capacity, the company was forced to terminate existing contracts with clients, resulting in substantial contractual penalties and the loss of customer relationships, as many clients excluded PKP Cargo from new tenders.

However, PKP Cargo’s new management, appointed by the Civic Coalition government in Q1/24, appears to be more competent and experienced. While the management board in place temporarily since January 2024 has reduced operating expenses and CAPEX and carried out the necessary layoffs, the newly appointed CEO, Agnieszka Wasilewska-Semail, who will officially take over on January 20, brings a wealth of experience. She has had a long and successful career in banking in both Poland and Belgium, as well as experience as the CEO of an industrial company undergoing restructuring.

Latest results

In its most recent full fiscal year 2023 (with the new Polish government in place since December 2023), PKP Cargo generated revenues of PLN 5.49bn (+1.9% y-o-y), with 75.8% from Poland, 10.7% from the Czech Republic, and 4.5% from Germany. The gross margin was 63% (compared to 58.7% in 2022), while the operating margin equalled 5.3% (down from 6.2%). Personnel expenses, at PLN 1.96bn, were by far the largest cost item. Net income amounted to PLN 82.1m (-44.5% y-o-y). Operating cash flow increased by 18.9% to PLN 1.21bn, but free cash flow declined from PLN 245.5m in 2022 to PLN 223.9m.

The first nine months of 2024 were very challenging for the company. A relatively weak economic environment in Europe and fewer orders from clients led to a 19.1% decline in revenues, which amounted to PLN 3.37bn. Germany was the only regional market where revenues saw a significant y-o-y increase (+29.1% to PLN 253m). Meanwhile, the gross margin improved slightly from 62.7% in 9M/23 to 63.4%, but the EBIT margin worsened from 6.2% to -23.5%, primarily due to a 53.2% increase in depreciation and amortisation expenses (including write-downs of rolling stock and other fixed assets). With a net interest result of PLN -142.2m (9M/23: PLN -133.3m), net income dropped from PLN 101.9m to PLN -795.7m.

As of the end of September 2024, PKP Cargo’s interest-bearing debt stood at PLN 2.85bn (compared to PLN 2.89bn on 31 December 2023), with 32.3% (up from 27.8%) of it being short-term. Net gearing rose to 99.7% (from 82.1%). Due to staff reductions, the PKP Cargo Group likely employed 16,268 people (down from 19,933 as of 31 December 2023). Following the signing of 17 letters of intent, subsidiariesof Polish State Railways (PKP S.A.) and other Polish companies have expressed their intention to hire around 2,500 of PKP Cargo’s former employees.

1. Rail freight is the most cost-effective and eco-friendly way to transport goods over long distances (one train can carry as much cargo as 64 trucks).

2. The European economy — particularly in Central and Eastern Europe (CEE) — continues to grow, driving demand for building materials, coal, fuels, and other goods.

3. Growth in the intermodal segment, which combines rail and road transport.

4. Technological advancements, such as GSM-R and GPS, enabling real-time tracking and monitoring of cargo from the point of loading to unloading.

Moreover, with significantly lower personnel costs expected this year and a disciplined approach to CAPEX spending, PKP Cargo’s current valuation of PLN 637m (compared to PLN 4.2bn at its peak in 2014) looks very attractive. We believe the company could generate an EBITDA of PLN 800m in 2025E (Sell-side estimate for 2024E: PLN 277m), which would imply an EV/EBITDA ratio of just 3.7x. The current P/BVPS stands at 0.27x, thus the company’s equity is almost 4 times higher than its current market capitalisation.

In terms of future investments, we consider the intermodal segment particularly promising and worthy of attention. Additionally, we expect PKP Cargo will need to invest in modernising its rolling stock and furthering its digitalisation efforts.